Student and Teen Checking

Want a teen account without the worry of overdraft and monthly service fees?

Look no further than Clear Access Banking.

Teens 17 and under must open at a branch.

Clear Access Banking – made with teens in mind

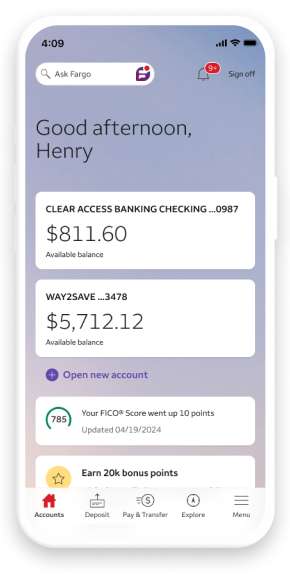

Convenient mobile banking

Zelle®, mobile deposit, and digital wallets help make teen banking easy.

No overdraft fees. Period.

Clear Access Banking is a great account to help teens manage their money and has no overdraft fees.

Avoid monthly service fees

No monthly service fee charged for primary account owners 13 - 24 years old.

Clear Access Banking details

- No overdraft fees

- Checkless checking account

$5 monthly service fee

- Primary account owner is 13 - 24 years old

- More ways to avoid the fee

- Must be 13 or older

- Teens 13 – 16 years old need an adult co-owner

- 17 and under must open at a branch

- IDs required to open

Everyday Checking - another option for students

Everyday Checking details

- Optional overdraft services

- Extra Day Grace Period

- Write checks

$15 monthly service fee

- Primary account owner is 17 - 24 years old

- More ways to avoid the fee

- Must be 17 or older

- 17-year-olds must open at a branch

- IDs required to open

Bank Easy

Get the app loved by millions

9M ratings | 4.9 stars

Bank Easy

Get the app loved by millions

9M ratings | 4.9 stars

*Screen image is simulated

**4.9/5 Stars on the App Store and 4.8/5 on Google Play as of July 1, 2024

Build strong financial habits that last

Open a Way2Save® Savings account and set up automatic transfers to help students reach their savings goals.

Learn how to create a college budget, build credit, and set goals with Wells Fargo's CollegeSTEPS®.

Access billions of dollars in higher education funding plus the strategies and tools to successfully navigate them at wellsfargo.com/scholarships.

Student Checking FAQs

How was your experience? Give us feedback.

Other fees may apply, and it is possible for the account to have a negative balance. Please see the Wells Fargo Consumer Account Fee and Information Schedule and Deposit Account Agreement for details.

If you convert from a Wells Fargo account with check writing ability to a Clear Access Banking account, any outstanding check(s) presented on the new Clear Access Banking account on or after the date of conversion will be returned unpaid. The payee may charge additional fees when the check is returned. Make sure that any outstanding checks have been paid and/or you have made different arrangements with the payee(s) for the checks you have written before converting to the Clear Access Banking account.

Minimum opening deposit is $25. Monthly service fee for the Everyday Checking account is $15 and can be avoided when the primary account owner is 17 through 24 years old. Monthly service fee for the Clear Access Banking account is $5 and can be avoided when the primary account owner is 13 through 24 years old. When the primary account owner reaches the age of 25, age can no longer be used to avoid the monthly service fee. Everyday Checking and Clear Access Banking customers have other way(s) to avoid the monthly service fee. Customers between 13 and 16 years old must open the Clear Access Banking account with an adult co-owner. See a Wells Fargo banker or the Consumer Account Fee and Information Schedule available at wellsfargo.com/depositdisclosures for more information about other fees that may apply and options to avoid the monthly service fee.

Our overdraft fee for Consumer checking accounts is $35 per item (whether the overdraft is by check, ATM withdrawal, debit card transaction, or other electronic means), and we charge no more than three overdraft fees per business day. Overdraft fees are not applicable to Clear Access Banking accounts.

The payment of transactions into overdraft is discretionary and we reserve the right not to pay. For example, we typically do not pay overdrafts if your account is overdrawn or you have had excessive overdrafts. You must promptly bring your account to a positive balance.

With Extra Day Grace Period, if your account is overdrawn, you have an additional business day (extra day) to make covering deposits and/or transfers to avoid overdraft fees. If your available balance as of 11:59 pm Eastern Time on your extra day is positive, the pending overdraft fees for the prior business day’s overdraft items will be waived. If your available balance as of 11:59 pm Eastern Time is enough to cover some, but not all, of the prior business day’s overdraft items, the available balance will be applied to the transactions in the order that they posted to your account (based on our posting order practices described in the Deposit Account Agreement). Any overdraft items that are not covered by 11:59 pm Eastern Time on your extra day are subject to applicable overdraft fees. All deposits and transfers are subject to the Bank’s Availability of Funds Policy. Please see the Wells Fargo Deposit Account Agreement for more details.

Mobile deposit is only available through the Wells Fargo Mobile® app on eligible mobile devices. Deposit limits and other restrictions apply. Some accounts are not eligible for mobile deposit. Availability may be affected by your mobile carrier's coverage area. Your mobile carrier's message and data rates may apply. See Wells Fargo’s Online Access Agreement and your applicable business account fee disclosures for other terms, conditions, and limitations.

Digital wallets may not be available on all devices. Your mobile carrier's message and data rates may apply.

Enrollment with Zelle® through Wells Fargo Online® or Wells Fargo Business Online® is required. Terms and conditions apply. To send or receive money with Zelle® both parties must have an eligible checking or savings account enrolled with Zelle® through their bank. Transactions between enrolled users typically occur in minutes. For your protection, Zelle® should only be used for sending money to friends, family, or others you trust. Neither Wells Fargo nor Zelle® offers purchase protection for payments made with Zelle® - for example, if you do not receive the item you paid for or the item is not as described or as you expected. Payment requests must be sent to enrolled Zelle® users. For more information, view the Zelle® Transfer Service Addendum to the Wells Fargo Online Access Agreement. Your mobile carrier’s message and data rates may apply. Account fees (e.g., monthly service, overdraft, Business Account Analysis fees) may apply to Wells Fargo account(s) with which you use Zelle®.

Availability may be affected by your mobile carrier’s coverage area. Your mobile carrier’s message and data rates may apply. Fargo is only available on the smartphone versions of the Wells Fargo Mobile® app.

You must be a Wells Fargo account holder of an eligible Wells Fargo consumer account with a FICO® Score available, and enrolled in Wells Fargo Online. Eligible Wells Fargo consumer accounts include deposit, loan, and credit accounts, but other consumer accounts may also be eligible. Contact Wells Fargo for details. Availability may be affected by your mobile carrier's coverage area. Your mobile carrier's message and data rates may apply.

Please note that the score provided under this service is for educational purposes and may not be the score used by Wells Fargo to make credit decisions. Wells Fargo looks at many factors to determine your credit options; therefore, a specific FICO® Score or Wells Fargo credit rating does not guarantee a specific loan rate, approval of a loan, or an upgrade on a credit card.

Wells Fargo and Fair Isaac are not credit repair organizations as defined under federal and state law, including the Credit Repair Organizations Act. Wells Fargo and Fair Isaac don’t provide credit repair services or advice or assistance with rebuilding or improving your credit record, credit history, or credit rating.

Turning off your debit card is not a replacement for reporting your card lost or stolen. Contact us immediately if you believe that unauthorized transactions have been made. Turning your card off will not stop card transactions presented as recurring transactions or transactions using other cards linked to your deposit account. Posting refunds, reversals, and credit adjustments to your account will continue. Any digital card numbers linked to the card will also be turned off. Availability may be affected by your mobile carrier's coverage area. Your mobile carrier's message and data rates may apply.

Terms and conditions apply. Mobile carrier's message and data rates may apply. See Wells Fargo's Online Access Agreement for more information.

Apple, the Apple logo, Apple Pay, Apple Watch, Face ID, iCloud Keychain, iPad, iPad Pro, iPhone, iTunes, Mac, Safari, and Touch ID are trademarks of Apple Inc., registered in the U.S. and other countries. Apple Wallet is a trademark of Apple Inc. App Store is a service mark of Apple Inc.

Android, Google Play, Chrome, Pixel and other marks are trademarks of Google LLC.

FICO is a registered trademark of Fair Isaac Corporation in the United States and other countries.

Zelle® and the Zelle® related marks are wholly owned by Early Warning Services, LLC and are used herein under license.

See the Consumer Account Fee and Information Schedule and Deposit Account Agreement for additional consumer account information.

Wells Fargo Bank, N.A. Member FDIC.

DT1-09162026-12-8599408-1.1