Sign On

Sign On May 2022

by Michael Swanson, Ph.D., Wells Fargo Chief Agricultural Economist

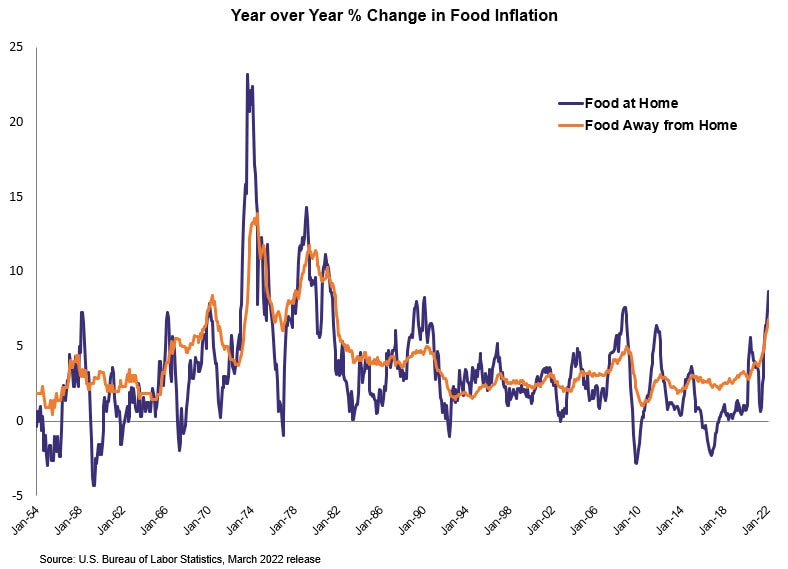

The current spike in food inflation has caught everyone’s attention, and it raises the question of how high, and for how long, will this inflation spike last? The graph below shows that food inflation is running at multi-decade highs.

The current spike in food inflation has caught everyone’s attention, and it raises the question of how high, and for how long, will this inflation spike last? The graph below shows that food inflation is running at multi-decade highs.

Clearly, the current rate of food inflation is not “the normal”. At the same time, looking at 70 years’ worth of data shows that there isn’t really a normal situation. Another important point to keep in mind is that “food” has evolved as radically as any other part of society over the last 70 years. Imagine the Twilight Zone where a food shopper from the 1950s is transported to today and steps through the supermarket door. They probably would only recognize a small number of the foods and beverages in the store. Those recognized would not only be in packages that astound them, but have superior quality and unfathomable labels. It becomes difficult to keep track of all the small changes that occur over a long period of time. People take the radical change for granted if it occurs slowly over a long enough time.

The above food inflation graph illustrates some important characteristics of the system that generates it. The competitiveness of the participants and diversity of resources make the price spikes sharp, but short-lived. Once the spike peaks, it typically is followed by a period of negative food price growth. The most recent price spikes were followed by one of the longest lasting and most negative periods of food deflation. Food manufacturers and food retailers continue to invest in automation and labor savings, making economies of scale important, and it shifts food away from the most expensive ingredient of all ― labor. Recent conversations with our extensive network of food manufacturers and retailers indicates they are accelerating their investments in automation and through-put capacity. But, their biggest challenges are lack of supply of equipment and expertise to install it. The battle for market share will continue to be a factor pushing competitive pricing following this inflation spike.

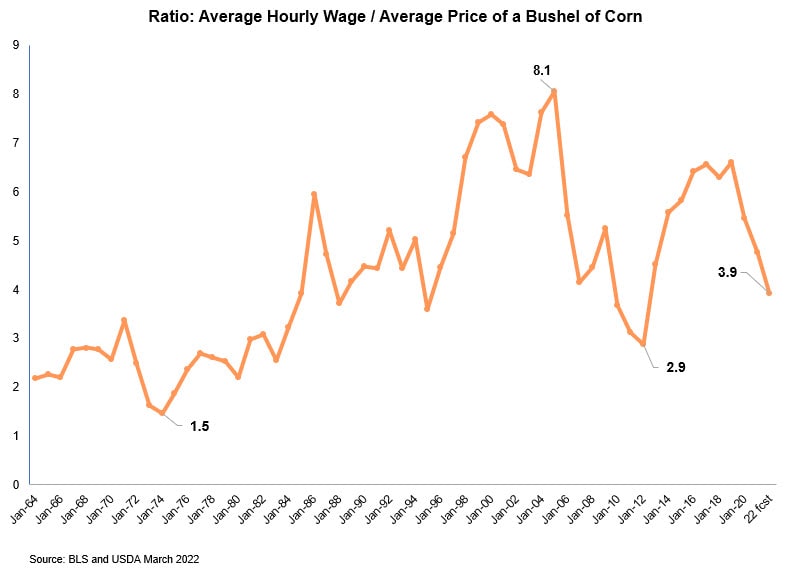

Another under-appreciated characteristic of the U.S. food system is that, over time, the raw ingredients typically get cheaper relative to wages. This results from the basic ratio of yield productivity growing faster than population growth. From the 1960s to the early 1980s, the average hourly earnings would have purchased 2‒3 bushels of corn. No one eats corn directly, but it supports production of sweeteners, eggs, meat, and dairy. Ultimately, it sets the real cost of food for many parts of the U.S. food system.

Starting in the early 1980s, corn yield productivity raced ahead of U.S. population growth, making it relatively plentiful and reducing its value relative to wages. In addition, the livestock industry became ever more efficient in their feed utilization. This relationship peaked in 2005 when the average hour’s wages would buy 8.1 bushels of corn. To put this into perspective, 8.1 bushels of corn contains more than a year’s worth of calories using the standard FDA 2,000 per day estimate. To say the least, corn was cheap, and it still is, using today’s prices and wages.

So, why the strong reversal in this corn to labor ratio from 2005 to 2012? In order to support farm income and returns, the U.S. introduced ethanol as a major new demand source that wasn’t tied to food consumption. And the Chinese economy was going through a once in a lifetime transformation that increased the demand for all commodities. Soybeans was one Chinese-supported commodity that accelerated with their growing and evolving livestock industry. Soybeans, as a competitor crop to corn, helped shore up the demand for the entire complex. This system transformation culminated with the 2012 drought pushing relative corn values back to the early 1980s, with a ratio of 2.9 bushels per hour of wages. With the build out of ethanol complete, and the Chinese expansion slowing, the relative value of corn reverted to more than 6 bushels per hour of wages. The U.S. food industry used this opportunity to expand sweetener, protein, and dairy expansion, pushing food inflation back into the negative range for a year, and helping to keep food inflation constrained until COVID disrupted the supply chains.

The COVID-induced inflation spike in 2020 was not about a lack of raw ingredients or even expensive ingredients. It was the cost of transformation that jumped based on missing employees in both the factories and the trucks to move them. This labor shortage showed up in all sorts of ways with freight rates, packaging, pallets, and other sundry component costs jumping based on spot shortages. Looking at 2022, the corn-to-wage ratio has moved back down (more expensive) based on the futures market’s risk pricing for Russia’s invasion of Ukraine. The most likely scenario is that Ukraine’s 2022 crop production will be lost to the war’s ruinous impact. Ukraine produced approximately 3% of the world’s agricultural output while having 0.6% of the world’s population. This allows them to be influential in the world’s grain markets with their exports. In contrast, my assumption is that Russia will plant its typical acreage and export it to countries with historically friendly relations. Many of those countries will not have any option other than to import wheat from Russia.

The traders and the futures markets are continuously churning through weather and world events to anticipate the next price in the market. There are so many moving pieces that it defies anyone’s ability “to be smarter” than the market. Investors and traders placing winning positions is different than being smarter than the market. At the moment, both the corn and wheat markets have started to discount the most severe scenarios, and futures prices have moved sidewise and slightly negative from their recent peaks. Of course, weather remains the single largest risk to production, and the North American grain and oilseed production is entering the key planting and growing season. Drought models and risks are always priced into the futures price. These elevated prices will be even more susceptible to weather volatility causing more risk in the near term, but the futures market has priced next year’s crop substantially lower than this year’s. This implies that food inflation will revert back to the pattern we saw in the first graph.

Will we see negative food inflation following this current spike? Well, it has occurred three times in the last twenty years following a spike in food inflation. The two largest drivers are: 1) the competitive nature of food manufacturing where economies of scale force a fight for market share, and 2) the yield growth of crops exceeding population growth. Both of these factors remain unchanged. In fact, 2021 population growth was 0.14%, the lowest since the contraction due to the Spanish Influenza in the early 1900s., In contrast, the blended yield gain for corn and soybeans in the U.S. has been 1.3% over the last twenty years. Even expecting population growth to rebound from impact of COVID, U.S. supply growth of grains and oilseeds will outstrip food demand growth. Without a repeat of introducing new demand from the transportation market, prices will be under downward pressure from increasing relative supply. With more employment in the factories and transportation sector, food inflation from the manufacturer level will also see a growth in supply and moderation in demand due to high prices. This seems to be setting the U.S. up to follow the see-saw pattern that has predominated for decades.

I can’t call the top of the current spike. No one can call the top the current spike due to the unforeseeable, but historical factors remain against food inflation lasting. Most historical food inflation actually represents better quality, convenience, and packaging for which consumers are happy to pay, when they shop. Still, we need to place our financial bets. I am betting the structure of the market remains intact no matter the state of the market. Consumers will be unhappy until these factors reassert themselves and food prices start to slow or reverse, and then consumers will take the cheaper food for granted, again.

Michael Swanson, Ph.D. is the Chief Agricultural Economist within Wells Fargo's Agri-Food Institute. His is responsible for analyzing the impact of energy on agriculture and strategic analysis for key agricultural commodities and livestock sectors. His focus includes the systems analysis of consumer food demand and its linkage to agribusiness. Additionally, he helps develop credit and risk strategies for Wells Fargo’s customers, and performs macroeconomic and international analysis on agricultural production and agribusiness.

Michael Swanson, Ph.D. is the Chief Agricultural Economist within Wells Fargo's Agri-Food Institute. His is responsible for analyzing the impact of energy on agriculture and strategic analysis for key agricultural commodities and livestock sectors. His focus includes the systems analysis of consumer food demand and its linkage to agribusiness. Additionally, he helps develop credit and risk strategies for Wells Fargo’s customers, and performs macroeconomic and international analysis on agricultural production and agribusiness.

Michael joined Wells Fargo in 2000 as a senior economist. Prior, he worked for Land O’ Lakes and supervised a portion of the supply chain for dairy products, including scheduling the production, warehousing, and distribution of more than 400 million pounds of cheese annually, and also supervised sales forecasting. Before Land O’Lakes, Michael worked for Cargill’s Colombian subsidiary, Cargill Cafetera de Manizales S.A., with responsibility for grain imports and value-added sales to feed producers and flour millers. Michael started his career as a transportation analyst with Burlington Northern Railway.

Michael received undergraduate degrees in economics and business administration from the University of St. Thomas, and both his master’s and doctorate degrees in agricultural and applied economics from the University of Minnesota.